INTRODUCING THE

CMV ALPHA COMMODITY 5 INDEX

The CMV Alpha Commodity 5 Index (“the Index”) is a rules-based index that aims to provide a synthetic long/short exposure to raw materials, looking to extract performance from the three main sources of alpha within commodities: Carry, Momentum and Value. To achieve this, its components consist of three dedicated BNP Paribas indices.

The Index can be classified as “All Weather”, as it seeks to provide resilient performance across different macro-economic regimes.

It uses a risk-parity allocation, aiming for the same risk contribution from each source of alpha, and integrates a volatility control mechanism that targets an annualized realized volatility of 5%.

For more information on the Index performance and statistics, please click here.

For a list of selected risks and considerations with the Index, please click here.

CMV ALPHA COMMODITY 5 INDEX FEATURES

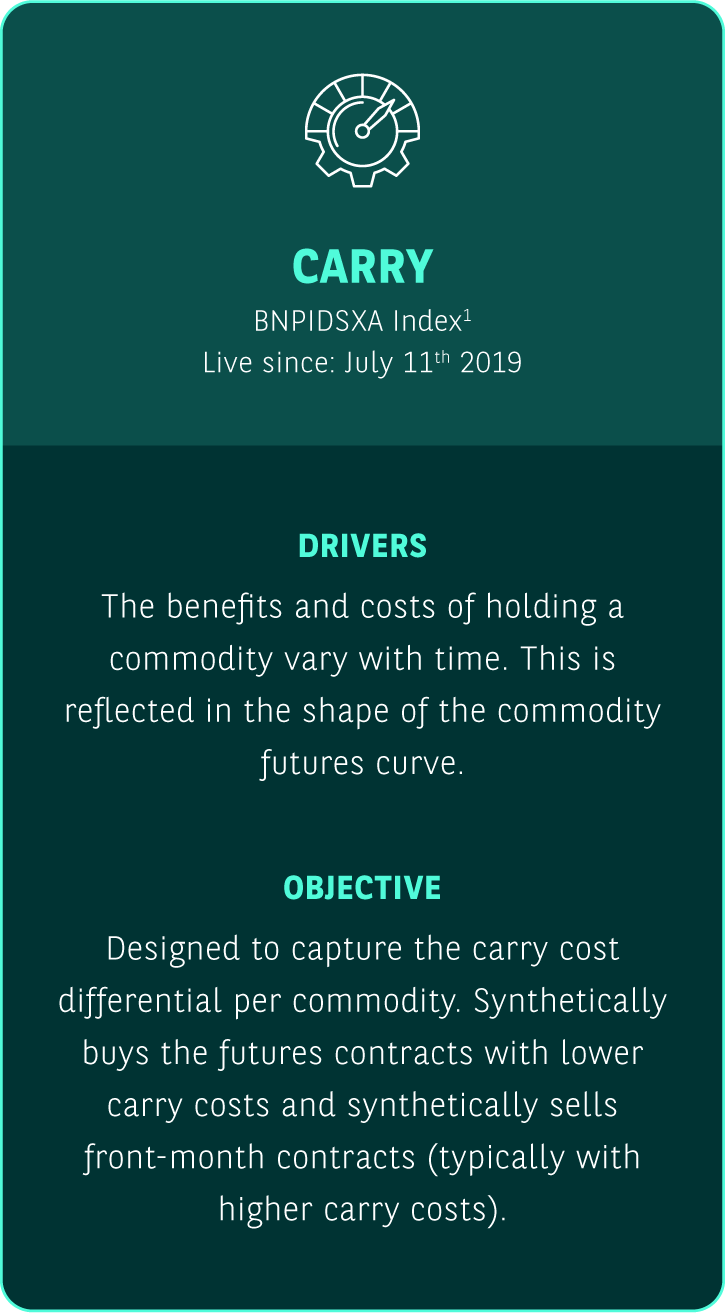

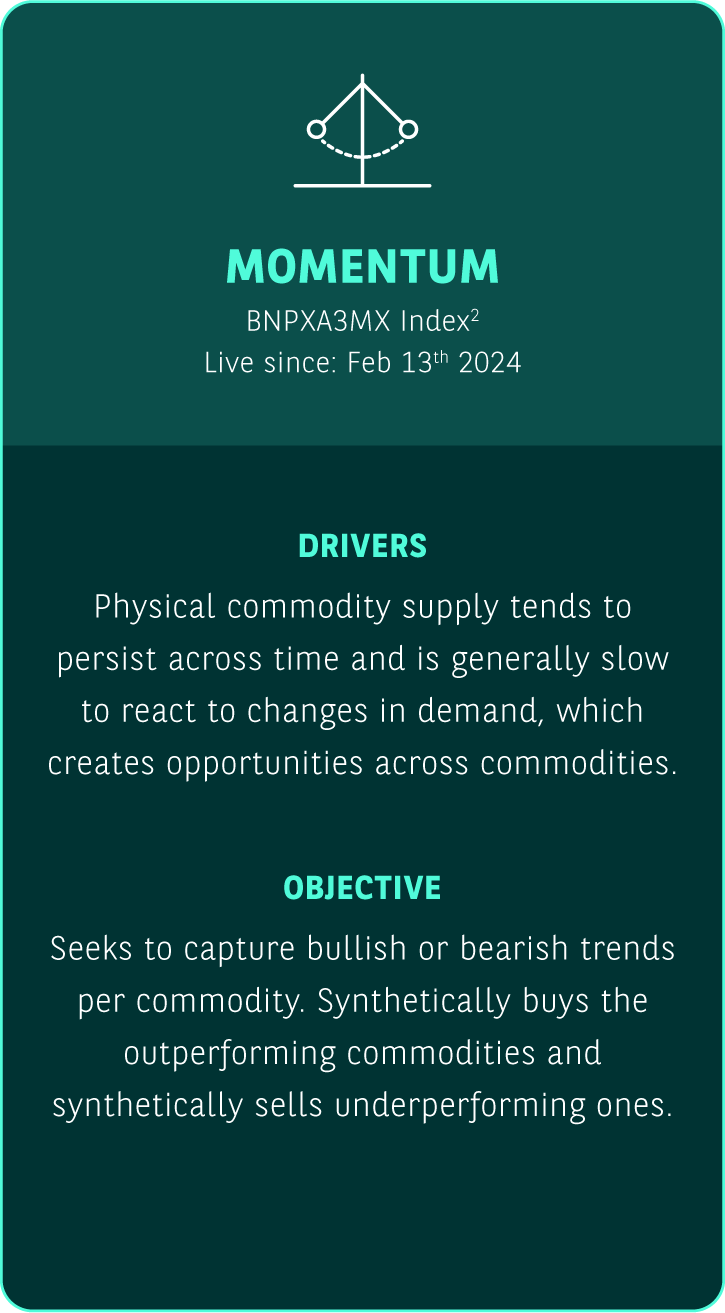

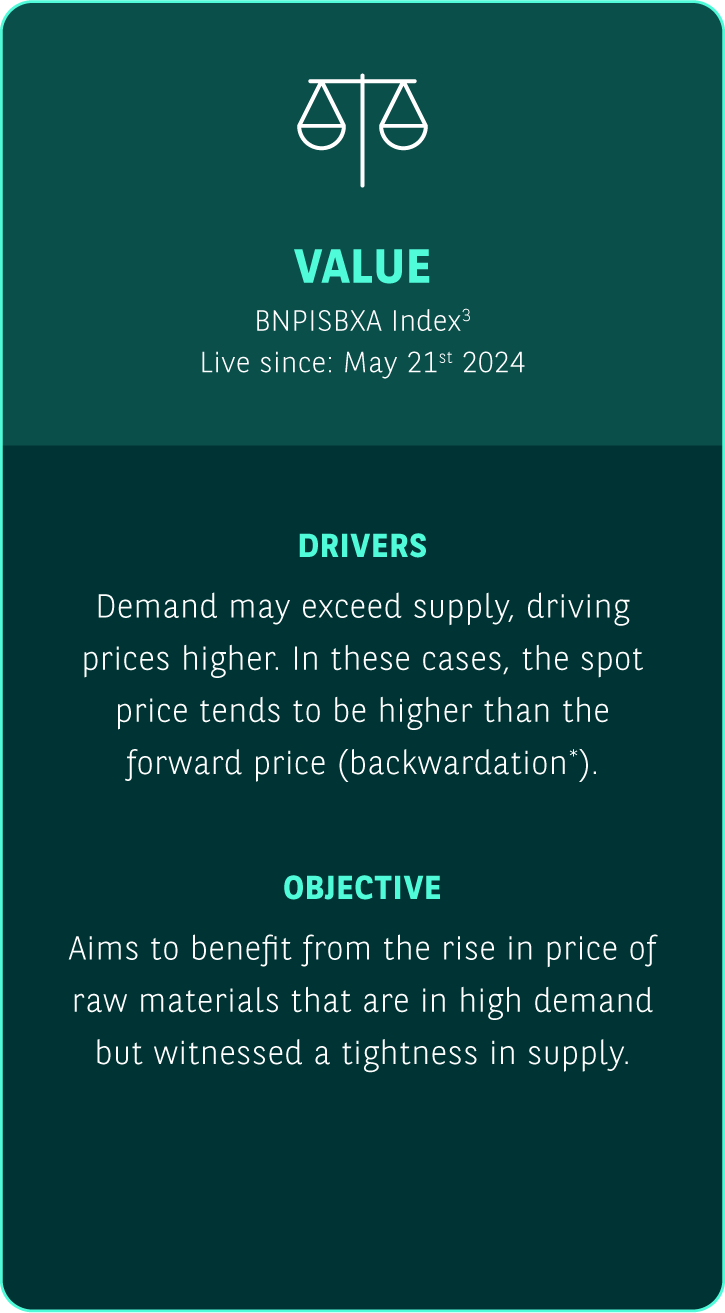

To extract performance from the three main sources of alpha within commodities, the Index is exposed to three dedicated BNP Paribas indices. Each of these indices are implemented within the CMV Alpha Commodity 5 Index through a synthetical long/short exposure with the aim to deliver diversified and uncorrelated performance across various market regimes.

However, each strategy is prone to underperform during regimes of heightened volatility in the commodity markets

1 BNP Paribas Commodity Daily Dynamic Alpha Curve ex-Agriculture and Livestock ER Index, Bloomberg code: < BNPIDSXA Index > , Live since July 11th 2019.

2 BNP Paribas Alpha Basis Momentum ex. A&L X3 ER Index, Bloomberg code: < BNPXA3MX Index >, Live since February 13th 2024.

3 BNP Paribas Time-Series Backwardation ex-Agriculture and Livestock Net Index, Bloomberg code: < BNPISBXA Index >, Live since May 21st 2024.

For information purposes only - Not for Further Distribution.

The CMV Alpha Commodity 5 Index aims to provide a well-diversi ed blended source of alpha that is not directly dependent on market conditions.

The Index is designed to provide:

• Low correlation to other assets

• Alpha extracted via a long/short position

• Diversified across sources of alphas

The Index is constructed through a risk parity allocation approach, aiming to balance the risk exposure across its components. This means that the components are weighted in such a way that the risk allocation of each of them is the same, giving less volatile components an equal opportunity to contribute to the overall Index.

After this allocation, a 5% volatility control mechanism is applied, adjusting exposure to the Index alongside a hypothetical cash component, with a maximum Index exposure of 250%.

DOWNLOAD MATERIAL

BROCHURE

An 10-page overview of the Index complete with performance information and definitions of key terms. Updated monthly.

FACTSHEET

A more concise overview of the Index, complete with latest performance information. Updated monthly.